A couple months ago, we took some of our own advice and got out there to do a bit of networking. We met with friends and former colleagues who’ve moved from consulting into ‘industry’ (companies that make and sell a product) – generally into strategy, insights, operations, project management or business development roles.

Here are 6 universal truths from our chats.

PROUD OF MY PRODUCT

Lots of people said that it’s really satisfying to point out what they do to friends and family. Grandparents understood the explanation “I work for a retailer” when they’d previously been bamboozled by “I’m a management consultant” or “I do corporate finance”.

DOING NOT ADVISING

A common frustration in professional services was feeling removed from the decision making and having to step away before any results were seen. In industry, people enjoy the feeling of “getting stuck in” and seeing the results of their efforts.

45 HOUR WEEKS

9 til 6ish is the average day for a corporate strategy or a business development position. Most had averaged 60 hours+ weeks in professional services – 33% more work!

A STEP SIDEWAYS IN £

Professional service firms pay you well. Don’t expect a big pay increase on joining (but you’ll probably earn more £s per hour). As a yardstick for you consultants out there; if you’ve 2-3 years experience you can expect £50k-70k basic salary working in a corporate strategy team (and yes, there is that much of a difference even within the same sector).

YOUR ‘IN-HOUSE’ ROLE CAN BE A STEPPING STONE

There’s a risk that because of your professional services background, you can get pigeon-holed as a ‘thinker’ not a ‘doer’. But if you’re keen on an operational role (e.g., buying, marketing, sales), use an ‘in-house’ job as a stepping stone. Network across the business and get involved asap with an operational project to prove you can do it! However, there are many networking mistakes that you should try and avoid. Set ‘operational experience’ as a goal in your appraisal and consider internal secondments. If you’re good, you can generally move departments within 2 years.

MAKES ME REALISE HOW LITTLE I KNEW OF THE INDUSTRY

Despite generally having done consulting projects in the relevant industry, everyone said it took them at least a year to get to grips with the detail of the business and the industry to the same level as their new colleagues.

If you liked this article, have a look at our other content related to moving in-house

You might – as a lot of people are – be in consulting as a means to an end.

They then step out – generally into ‘industry’, be that a global corporation or a new start-up – and lots (thousands of top-tier consultants worldwide) discover their next global, perm or freelance opportunity having become a movemeon member.

A while later you’re looking up towards the more senior roles and thinking ‘that’s not for me’. Perhaps you want to really ‘own’ a product/P&L/business unit – stepping into more of a ‘doing’ role than an advisory one. Perhaps you’re fed up with the long hours & travel.

Either way, you’ve decided you’re not sticking around forever.

So, what is the right point at which to leave consulting?

At this point, I’d like to say that loads of people love consulting and stay in the industry for a long time – perhaps their whole career. They have a great time and love their work. And there’s absolutely nothing wrong with that. In fact, it’s fantastic when people discover a career they enjoy and this scenario is true of a lot of my friends who started with me in consulting and are still there having made Partner.

This article is premised on using consulting as a means to an end.

It is designed to help those people who get in touch with us having made the decision not to stay. It is not designed to make people who stay longer feel like they ought not to have!

Please don’t take what I say now as complete gospel. There will be plenty of people who’ve left consulting at different points to the ones I reason below and gone on to be hugely successful. There is no golden rule or silver bullet so you shouldn’t feel like you’ve got it wrong if you’re not following the path below. This is just a summary of the sentiment we commonly pick up from the 1000s of employers who get in touch to use movemeon. And that summary is that the perfect time to leave is between 21 and 30 months – or more readily stated as just less than 2 years up to 2.5 years or so. You might be looking for the perfect opportunity right through that window.

Why are employers seeking consultants with this level of experience?

Here are the common reasons:

After about 2 years, you’ve probably developed all the transferable skills that they’re after and that you went into consulting for. So employers see diminishing returns for staying in consulting longer. What do they get from a 3ish year consultants that they can’t get from a 2ish year one?

Instead, what they want now is genuine industry expertise and the best way to develop that is by working for them. As much of an industry expert as you might think you are thanks to a couple of consulting projects, most consultants who move into industry say that it took them about 1 year to REALLY get to grips with all the detail of the industry and the business.

You’re affordable. At the more junior levels, consulting salaries generally ramp up faster than industry salaries. The industry then catches up from Manager onwards, particularly thanks to share schemes. So, if you’ve been in consulting for 3-4 years – say to Senior Associate to Junior Manager level – your expectations on salary will be beyond the worth that industry puts on you (thanks to points 1 and 2 above).

If you miss the 2-2.5 year window, it doesn’t mean that you’re not going to get a good job outside of consulting.

It does probably mean that you’ll need to adjust your expectations down in terms of salary and responsibility. Simply put, you won’t get offered a job that isn’t also offered to someone in the 2-2.5 year window.

This can apply right up to Manager level

Particularly if you’ve been managing for 6-12 months. Yes, you may have gained managerial experience in consulting. But realistically, because you are not an expert in the detail of their business/industry, employers can’t credibly employ you to step in and manage teams in their business. You’d probably have to come in, with a view to / understanding that you’ll be promoted quickly.

So if you’ve just been promoted to Manager, right now is a good time to be looking (and if you did an MBA, you’re probably in the 2-2.5 year window anyway). If you decide to stay for longer as a Manager, it’s better to do a couple of years and really focus on an industry and/or a function (pricing, sales, supply chain etc). That way you can more credibly move into a Manager level role in that industry and the greater responsibility & salary that comes with it.

But that probably means doing about 5 years total in consulting so make sure you’re prepared to stay for that longer haul! Also, there’s nothing to say that you wouldn’t have reached that level in the industry sooner, had you left consulting in the earlier window (depending on how good your new company is at promoting rising stars).

Our new product Payspective is fully dedicated to creating benchmarks and insights around pay, career progression, working hours and more. Follow Payspective on LinkedIn or sign up to our newsletter.

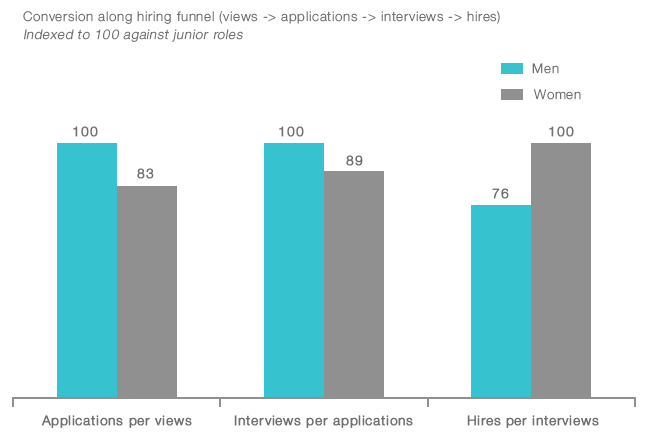

Women are 36% more likely to be hired than men – but they are also far less likely to view a job and then apply. Men compete more but win less.

Our labour market, more so than ever before, is shaped by people moving between jobs. We, therefore, wanted to understand how our members were behaving on movemeon. Having analysed over 20,000 applications, we were fascinated to see some clear trends. Women were not only more likely to be invited to an interview after an application, but they were also then performing better at these interviews. As such, we found that each application made by a woman is 35% more likely to result in a job hire than a man.

In this article, we look through the potential causes of these differences at each stage of the hiring cycle (discovering jobs; applications and interviews). Whilst we put forward some solutions, we want this article to be the start of debate – both internally here at movemeon and also externally in the industry. What can employers and society do to address the imbalance in discovery and applications?

The analysis

We looked at the “hiring funnel” for all of these job applications: from viewing a job to applying, to interview, to being hired. Comparing the different conversion rates at each part of this funnel yielded some very interesting results. Not only did women view 20% fewer jobs than men, but they also appeared less likely to apply after viewing a job: on average women would view 25% more jobs before making an application than a man.

Having made these applications, the conversion to interview was 12% higher for women: in short, their applications were better. Women are also an astounding 24% more likely to be offered a job after having been interviewed.

The end result: after having made an application, women are 36% more likely to land the job than men. In essence, men are competing more but winning less.

Casting the net: why women apply to fewer jobs than men

Before choosing to view a job in full on movemeon, candidates are only able to see the following: salary, industry, function, a hook selling the job, and location.

Our first hypothesis is that salary might put women off applying more than men. Men seem to be more open to taking a risk on salary than women, based on our analysis of submitted salary expectations attached to applications. We found that women were asking for only 85% and 92% of the salaries men were expecting in corporate and startup jobs. This may also be true with respect to location, and relevance of skill set vs. new industries and functions.

Secondly, it might be that the marketplace has more opportunities that are more popular with men than women (i.e., higher risk start-up jobs, tech jobs and operations functions). These industries have traditionally struggled to attract as many female applications and could be the cause of uneven views of jobs.

Finally, might it be that the language in the ‘hook’ lends itself to a male audience? Often the hook is a punchy challenge; an invitation to stretch yourself. If women are, as studies have suggested, less aware of their potential than their male counterparts, it could be that jobs advertisements are systematically written to appeal to the male psyche.

Putting your hat in the ring: women apply less frequently having viewed a job

I would suggest that similar factors could be at play in the decision to apply for a job from a view. This would have the double effect of decreasing the number of female applications, but also increase the percentage of successful applications. If women do apply when they are surer of a fit with their current skills, they are more likely to be invited to interview.

The higher number of views per application also suggests a more measured approach. Women are taking longer to investigate, and therefore both find roles that are a good fit as well as properly tailor applications.

Performance at interview: women are 25% more likely to be offered a job

As noted earlier, the real difference comes at interview. Women are more 25% more likely than men to be offered a job after an interview.

This is a fascinating insight, as traditionally interviews have been seen as an area again contributing to an imbalance in recruitment. Linda McDowell writes in her book Capital Culture: Gender at Work in the City: ‘recruiting is an interesting area to consider in examinations of gender stereotyping as it is at this stage that the particular characteristics and attributes sought in potential employees are made most clear’. Undeniably, at times these expectations still disproportionately favour men.

Fundamentally, women are the better candidates at interview. The key driver for this could potentially be the better quality of applications at the initial stage of the hiring funnel: this has flowed through in each step until the decision to hire is made.

How can employers encourage more women to apply for jobs?

McKinsey have estimated that adding women to the workforce to the ‘best in region’ levels would add $12 trillion dollars to the global economy. It goes without saying that getting women to parity in the labour market should be a social priority of the highest order because it is unquestionably the right thing to do. As if any more incentive was needed, $12 trillion is a number utterly beyond comprehension.

How then, can employers remedy this and improve their hiring at the same time? After all, more fairly weighted an application process is the more competitive it will be, and competition breeds the best hiring. We suggest:

Survey women to get a better understanding of what they are looking for in a new job, and thus in a new job description.

Specifically, explain that the business is actively targeting women (e.g., explaining about women leadership programmes; what’s provided to help manage a dual-life)

Test what actually works: as we always find, adding data helps remove ambiguity. Test different hooks, salaries, etc. and run different ads to A/B test (we’re starting these up at movemeon).

Look to take more women through to interview (target a 50:50 short-list for all roles). Our analysis suggests they put higher levels of consideration into applying and are outperforming men at interview!

Some quotes to leave you with

Warren Buffet’s article on gender and the labour market, inspired by Sheryl Sandberg’s Lean in, addressed some of our most entrenched social issues. Here are some key takeaways:

Stop holding yourself back

“I’ve seen very, very bright women. I use the example of Katherine Graham. While she was CEO of The Washington Post, the stock went up [by a lot]. She won a Pulitzer Prize. But she’d been told by her mother, she’d been told by her husband, she’d been told by lots of people that women weren’t as good as men in business. It was nonsense.”

“And I kept telling her, you know, ‘Quit looking at that funhouse mirror. You know, here’s a real mirror. You’re something.’ And as smart as she was, as high grade as she was, you know, as famous as she became, right to her dying day, you know, she had that little voice inside her that kept repeating what her mother had told her a long time ago. So everybody should get a chance to live up to their potential. And women should not hold themselves back. And nobody should hold them back. And that’s my message.”

Demand equal pay

“I do very little negotiation with people. And they do little with me, in terms of it – if I was a woman and I thought I was getting paid considerably less than somebody else that was equal coming in, that would bother me a lot. I probably wouldn’t even want to work there. I mean, [if] somebody’s gonna be unfair to you, in salary, they’re probably being unfair to you in a hundred other ways. I mean who should you spend your time with?”

Make yourself known

“[One woman] told me that she went to Harvard Business School. The women just didn’t raise their hand as often as the men. I raise my hand all the time. When I didn’t even deserve to. So you wanna get over the idea, as I wrote in the [Fortune] article [that] there’s a lot of Wizard of Oz in us. I mean, you get behind the curtain and you’ll find out that it wasn’t quite that imposing.”

Know the power of your potential

“Look what’s happened since 1776, most of the time, using half our talent. I mean just imagine what’s gonna happen when we, you know, go full blast with 100%. And you know, it’s incumbent on everybody to try and help people – particularly if you’re in a boss’s type position, to help the people achieve their potential. And women have every bit the potential men do.”

Subscribe to our monthly newsletter to receive our latest insights, career tips, and industry experts interviews straight into your inbox:

The private equity series is a collection of articles written by Quentin, MMO member who moved from consulting to private equity through Movemeon. We distribute our new content (like this article) on Linkedin. Follow us and never miss out on insight, advice and events. Or you can register to gain access to our weekly newsletter.

You can find the others articles of the series here:

Deciding to set sail for the world of private equity (‘PE’) is unfortunately not enough to get a role in this industry. The job market remains highly competitive in this area and, as for any investment. A PE firm will only hire someone if it believes the value the new member adds is (much) greater than its cost. As a strategy consultant, there are nonetheless a handful of clear windows of opportunity where your experience and your skill set make you a ‘good bargain’.

In a nutshell, the role you aspire to will be the key driver of your timing. To summarise, there are three main paths you can follow:

Become part of the deal team as an investment professional. This is the most common decision and here the answer is actually relatively straightforward. You should aim to jump ship as early as possible. Indeed, the skill set you will typically develop in consulting is of limited relevance for PE. Thus, the longer you wait the more significant the skill gap with investment bankers (competing for the same jobs) will grow. That being said, almost all PE firms tend not to hire anyone with less than 2 years of experience. A good way to make the most of this period is thus to join a ‘private equity taskforce’, i.e. a ring-fenced team dedicated to executing strategic and operational due diligences. Many of the largest consulting firms do host this kind of structure. In any case, applying for a deal team role will require you to bridge the skill gap that will remain in spite of everything, in particular with regards to financial modelling and structuring. A word of caution though: this path is clearly ‘high reward but high risk’ in the sense that your task force experience will represent a competitive disadvantage if you ultimately decide to change your mind and follow a more traditional corporate path after your time in consulting.

Join the operations team. Over the last few years, the largest PE houses have created teams that focus on strategic and operational aspects of the due diligence and/or the investment management processes. KKR Capstone, Bain Capital and Clayton Dubillier & Rice are often quoted as pioneers on that front. The operational team should offer a complementary skill set compared with the one in place within the investment team. As a consequence, PE firms are particularly looking for professionals with a total of 7-10 years of experience mixing consulting and operational roles, although the latter is optional. In practical terms, you could envisage to either progress your consulting career up to the stage of Principal or leave once you are a Consultant/Project Leader and join a company, either in a strategy or a line management role. Paradoxically, being a Partner decreases your market value since PE firms are interested in project managers – not sales persons.

Act as senior adviser. PE firms often rely on pools of very experienced industry professionals to set their Boards of Directors and to possibly fill a vacant CEO role on an interim basis. Moreover, former executives tend to have created a quite distinct network which will nicely complement the one deal teams have. This thus leaves the door open for a “Partner + CEO and/or Board member” path – not the shortest or the most straightforward I have to admit.

Conversely, you can identify periods of your consulting career when a transition to PE will be sub-optimal, if not impossible. Most notably, an experienced consultant on the verge to being promoted to Project Leader suffers from the worst of two worlds: too experienced (with the wrong kind of experience) and too expensive to become a deal professional but not proven enough to manage people and projects as part of an operations team. This general framework should not occult the fact that each PE firm has its own idiosyncrasies and that the best way to prepare for a transition to this industry is to meet as many people as possible within the environment you target – refer to my first post to narrow down your search. In any case, the sooner you start this process, the higher your chances will be.

The private equity series is a collection of articles written by Quentin, who moved from consulting to private equity through movemeon. We distribute our new content (like this article) on Linkedin. Follow us and never miss out on insight, advice and events. Or you can register to gain access to our weekly newsletter.

You can find the other articles of the series here:

I would like to pursue this series of posts on private equity by debunking a myth which represents private equity as a ‘graal’ with only advantages compared with the life in consulting. Although life as a private equity professional can be considered as a ‘step forward’ in many respects, several aspects of the job may be worth considering before making a move to a fund (more on this in this article). The list is split into three categories: ‘pluses’, ‘equals’ and ‘minuses’.

PRIVATE EQUITY WINS

Compensation. The package is often designed to attract investment bankers, who are better paid than strategy consultants. As a consequence, you should expect a significant increase of your total compensation package, up to 100% in some cases. Larger funds are usually more prodigal – the assets under management per head ratio grow with the size of the fund – but this tends to come with a heavier workload as we will see later on.

Ownership. The role of a consultant is by definition to provide advice on a (most often) narrowly-defined topic. This role can be frustrating given that (i) the consultant usually does not know whether his recommendations were ultimately implemented or taken into consideration and (ii) the consultant cannot address an area for improvement outside the scope of work, no matter how promising and easy to sort out this area could be. Conversely, the private equity professional adopts a holistic view of the company and pragmatically works with management teams on the points which offer the best return on investment (both time and money). Incentives (through carried interest and management equity) should be designed in order to align interests.

Adrenaline. Linked to the point of ownership, closing a deal which you have owned is much more rewarding – many professionals mention the ‘adrenaline shot’ – than closing a consulting project whose future is uncertain.

Relationship with management. As a consultant, the management team is your client, and you need to seduce the team to rally them to your cause at the beginning of the project (otherwise you may face endless pushback to get the data you crucially need for your analysis) and to try to sell a follow-on project (ideally a massive implementation work) once the project is over. This partly explains why many talented Principals fail to make it to Partner: the nature of the job changes, from project manager to business development agent. Commercial considerations may consequently have an impact (even unconsciously) on the quality and conclusions of your work – if you solve all the issues in Phase 1, what will you work on in Phase 2? The private equity approach again goes ‘straight to the point’. During my 2 years at TowerBrook, I have never produced any PowerPoint document for discussions with management – back of the envelope calculations and Excel spreadsheets were all we needed.

Timeframe. Consulting projects are squeezed into 4 to 8-week periods, a timeframe which is often too short to fully explore the issues in-depth and build truly open relationships with your counterpart – who often ends up the project half-traumatised by the speed of change and permanent sense of urgency. Private equity firms hold companies for 4 to 7 years and can thus enforce a slower pace – losing a day or a week is less crucial. The quality of relationships naturally improves as a consequence.

Multitasking. Consultants work on one project at any given point in time, whereas private equity professionals frequently cover 2 or 3 portfolio companies – sometimes even more. In the latter case, you can pick your battles and produce the effort where the reward exceeds your cost (i.e. your salary). Conversely, consultants need to fill their diary even during project downtimes, which can give rise to low-value-added tasks – a waste of the consultant’s time and the client’s money.

Exposure. As a shareholder representative, you benefit from even wider access to senior management compared with your strategy consulting experience – when you are a junior in consulting you mostly interact with mid-management, in private equity you can navigate throughout the organisation. Private equity also introduces you to Board meetings, whose dynamic generally represents a good learning experience.

Exposure (cont’d). Being a strategy consultant enables you to meet a lot of individuals, but 90% of those individuals will be co-workers with the same type of background, the same concerns and the same professional aspirations as you. Trying to broaden your network beyond this circle is very often difficult: you do not have the time and little to offer to your prospective interlocutors. On the contrary, private equity is all about networking so you are encouraged to meet bankers, consultants, managers etc. and possibly source your own deals from day 1. Not only does it make the day-to-day experience more enjoyable, it also enables you to build an ‘intangible asset’ you will be able to use all your life.

Career path. In big established consulting firms the career path is well established and predictable and everyone can expect to make it to Partner if his individual performance justifies it. In private equity, the performance of the fund as a whole, which you do not have full control on by definition, also drives career tracks. In one hand, a growing fund (in terms of assets under management) will need to reinforce its human structure and may create early opportunities for promotion. On the other hand, senior positions in a stable or declining fund are most often already filled by the ‘first wave’ of professionals. Given the low churn in this industry, a junior joining one of these firms will struggle to make it to the top – hence thorough due diligence is key prior to joining the firm, see one of my earlier posts on the topic.

PRIVATE EQUITY AND CONSULTING ARE EQUAL

Variety of topics. Large consulting firms will provide juniors with an unchallenged width of experience. Within the first two years of your career, you could work on a reorganisation for a bank, on a strategic review for an oil producer, on a pricing project for a food retailer and on a supply chain mission for an automotive manufacturer. In private equity, you may end up investigating more opportunities but will only focus on a handful. Each individual should assess which approach better suits him.

Level of issues. In both cases, you will deal with high-level strategic issues as well as operational concerns.

Learning curve. Both environments offer an amazing learning experience with very few equivalents. Strategy Consulting will provide you with the tools to think about an issue, perform the relevant analysis and formalise and communicate recommendations in a simple but convincing way. Private equity will confront you with the real life of business and will overlay financial considerations – companies can only exist if they make a profit, there is no way around it.

Travel. Travelling Monday to Thursday as a consultant is not fun, but private equity professionals are also very often on the road. Trips are usually shorter and more frequent, which means that you will probably spend more nights home but you may end up more tired.

Work/life balance. In strategy consulting, you should expect to work relatively hard but the workload tends to be relatively smooth over time. In private equity, you can have very quiet periods followed by very intense weeks when your team is working on a deal. The ‘peaky’ nature of workload is similar to the one investment bankers face.

Opportunities. Both worlds open a vast array of opportunities, although within slightly different worlds – consulting is more generalist and corporate-orientated whereas private equity tends to form a ‘self-contained’ world.

STRATEGY CONSULTING WINS

Job stability. As mentioned earlier, in strategy consulting, if you do your job properly, you can build a career with high certainty. In private equity, external elements interfere.

Chemistry. Consulting firms are made of hundreds of consultants, so the absence of ‘chemistry’ within a project team is not a big issue – the lineup will be reshuffled for the next project. In private equity, the team is rather small – 30 investment professionals at most, with a median of 5-6 – so the ‘human factor’ is key. The sword is double-edged: it can make your experience really great but could also spoil it in a very short timeframe.

Variety of task. In strategy consulting, projects may have very different objectives and as a consequence, the approach the team will adopt and the nature of your own work as well as the tools you will use may completely change from one project to another. Conversely, the private equity ‘toolbox’ is more limited, although a good professional will learn to apply this toolbox to a wide range of industries and contexts.

Training. Formalised training is something you will not get in private equity, so I strongly encourage you to make the most of the very well-conceived training modules during your life as a strategy consultant – even if it means waking up an hour earlier on a Friday to have time to finish your presentation before heading to the training room. Similarly, very few private equity firms have a culture of systematic, open and honest feedback as developed in many consulting firms. You should be even more proactive to ask for advice and guidance if you want your private equity career to be a success.

Again, this list only represents my perception based on my own experience and the numerous conversations I had with industry insiders. Each individual will have his own view, and each fund will offer its own ‘package’, hence I am obviously open for comments – comments which you can formalise by sending me a message on Linkedin.

Subscribe to our monthly newsletter below to receive our latest insights, career tips, and industry experts interviews straight into your inbox:

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

Strictly Necessary Cookies can include cookies to improve your security set by our third-party partners Sucuri and Cloudflare.

3rd Party Cookies

We use third-party cookies to understand how customers use our services and to send targeted ads. Some of our third-party partners use localStorage as part of tracking.

We use retargeting and marketing cookies to send our users relevant ads and content. We use third-party for this purpose for retargeting via Facebook, Linkedin, Google Adword, AdRoll and other similar applications. Emails and marketing campaigns using Outfunnel, Pipedrive Web Visitors and Mailchimp.

Keeping this cookie enabled helps us to improve our website.